.avif)

Stablecoins have quickly become an integral part of the digital asset ecosystem with a market cap of $222.16billion (Forbes ). Stablecoins have the potential to revolutionize corporate treasury operations, offering transformative solutions to long-standing problems with liquidity management, cross-border payments, and operational efficiency.

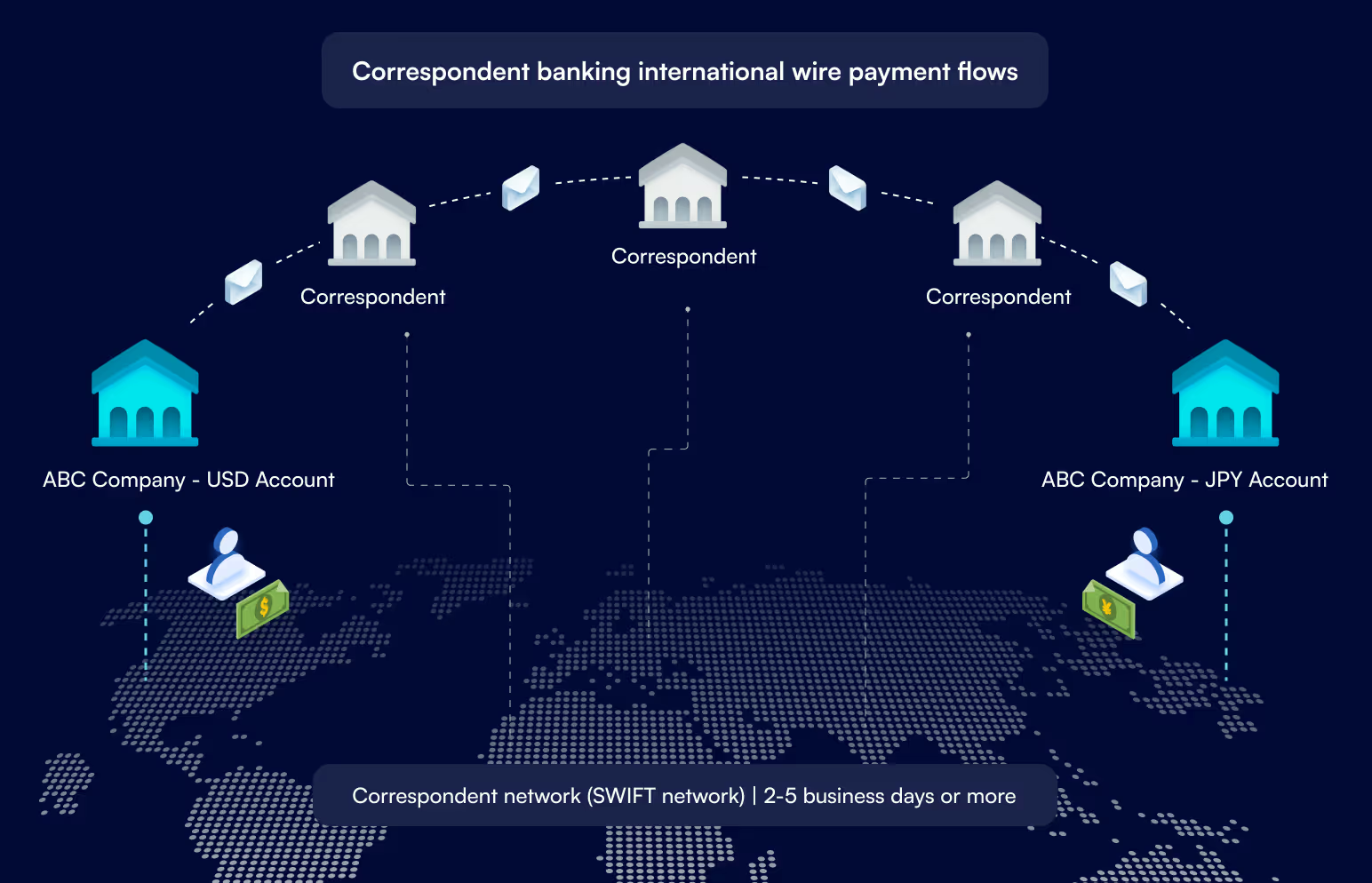

Corporate treasury teams often have pre-funded foreign currency accounts or multi-currency accounts to facilitate cross-border payments. These accounts hold balances by a company’s bank in another country to ensure local currency is on hand for payouts.

These balances are frequently rebalanced. Treasury teams monitor payment flows and top up or draw down foreign currency accounts as needed to keep sufficient funds available. This has been an essential process for corporations to meet customer expectations, however, itis labor-intensive and hindered by cutoff times and forecasting inaccuracies.

Corporate treasury teams deal with several significant issues managing liquidity and facilitating cross-border payments:

Additionally, the less common the currency pair, the more correspondent banks are required to make the payment, increasing fees and delays throughout.

At each bank in the payment flow, the following happens:

In order for the funds to move from one account to the other, the domestic payment systems for each must be accessed during normal business hours. The sender’s bank will need to hold enough cash to cover these unknown costs until the payment is complete.

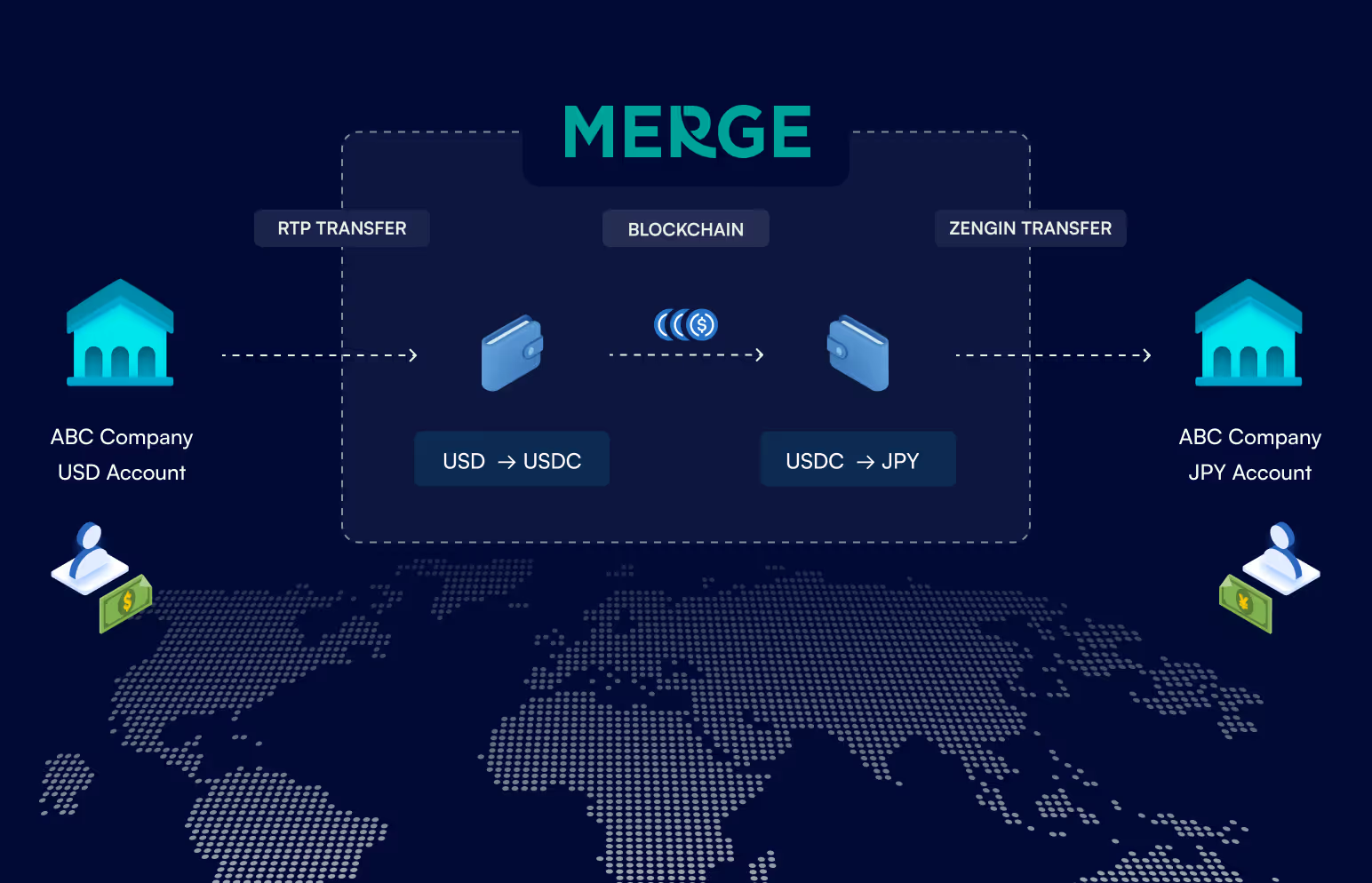

Stablecoins can offer a streamlined approach to address these challenges:

For stablecoin funds to move instantaneously from a digital wallet to a local bank account, they must be processed through regional instant payment rails. While over 80 such systems currently operate or are under development globally - including SEPA (Europe), Faster Payments (UK), PIX (Brazil), and UPI (India) - their reach remains limited compared to the traditional SWIFT network, which provides connectivity across more than 200 countries and territories.

These instant payment infrastructures, though growing in adoption, have yet to achieve the comprehensive global coverage that characterizes the more established SWIFT system.

As stablecoin adoption continues to grow, regulators are developing frameworks to ensure stability and consumer protections. This is not global yet which is a challenge that needs to be overcome.

In the US, the “GENIUS Act of 2025” aims to implement a regulatory framework for “payment stablecoins,” allowing issuance by permitted entities under federal or state supervision. The UK is moving towards regulating stablecoins under existing e-money regulations, with the Financial Conduct Authority (FCA) as the leading regulatory body. The EU’s Markets in Crypto-Assets (MiCA) framework establishes guidelines for stablecoin payments, requiring issuers to partner with licensed financial institutions.

Further adoption and innovation around stablecoins with emerging technologies are creating exciting opportunities. Businesses are exploring and developing programmable money concepts for automating treasury functions, supply chain finance, and international trade settlements.

Stablecoins represent a paradigm shift in corporate treasury management, offering solutions to age-old challenges in liquidity management, cross-border payments, and operational complexity. As the regulatory landscape continues to evolve, treasury management teams with a forward-thinking approach have the opportunity to utilize stablecoins to drive significant operational efficiencies and improve their companies’ financial performance and strategic agility.

Disclaimer: This content is intended for informational purposes only. It should not be considered financial, legal, or operational advice. Businesses should evaluate their own compliance, regulatory, and infrastructure requirements before implementing payment solutions.